NYSE MAC Desk

Fed Recap:

STRAIGHT FROM THE TRADING FLOOR

by Michael P. Reinking, CFA & Eric Criscuolo

DOW 51,594 (-1153), S&P 500 7,316 (-113), Russell 2000 2,906 (-47), NYSE FANG+ 16,567 (-210), ICE Brent Crude $90.81/barrel (+$6.72), Gold $4,060/oz (+$21), Bitcoin ~63.5k (-423)

- Fed leaves rates unchanged

- Still committed to 2% and no forward guidance

- Markets doing some of the work

- Yield curve steepens

- Equities sell off

MAC Desk Commentary:

Heading into this meeting, for the first time in a long time- at least since 2022- there was a real question as to what action if any the Federal Reserve would take. Since the last meeting inflation data came in better than expected and the labor market data also moderated. Rates had initially moved lower in response to that data. However, as oil prices moved higher with the escalation in Iran rates rose and calls for a hike at this meeting grew louder. The overwhelming majority believed the central bank would leave rates unchanged, a hawkish hold. Ultimately there was no rate increase and the language in the statement was also unchanged. After the unanimous vote in his first meeting there were three dissenters who preferred a 25bp rate hike, representing the family feud he referred to throughout the press conference.

Like the Fed’s statement the MAC Desk will also shorten up its Fed Recap. Notably the Chair didn’t repeatedly answer questions with “we’ve got a task force for that”, so there's a very sober audience out there. During his prepared comments Warsh highlighted the recent move higher in real yields, which he noted was one of the largest intra-meeting on record, suggesting this was in part due to a removal of forward guidance. As you can see he's closely watching the MAC Desk watch markets.

Warsh later implied that this tightening of financial conditions was doing some of the Fed’s job for them. The markets initial read was dovish with yields, particularly the 2yr, moving lower (partially positioning-related) and equities rallying. However, 10 and 30y yields started to move higher during Q&A, when reporters began to zero in on 1) the inflation framework, including how its measured, and 2) “what are you waiting for” to hike rates. For the former, Warsh paid homage to the PCE as the objective function and forcefully committed to the 2% target, before adding “who knows what we might say come January about strategy” after the task force weighs in. The “what are you waiting for” questions were answered with a mix of commentary on the market doing a lot of tightening on its own over the inter-meeting period and pointing back to the task force again. Neither provided a definitive answer, and the long-end responded by discounting more path uncertainty and potential for the Fed to fall behind in its inflation fight- not like it was in the lead. The 30y breached 5.20%, back to YTD highs.

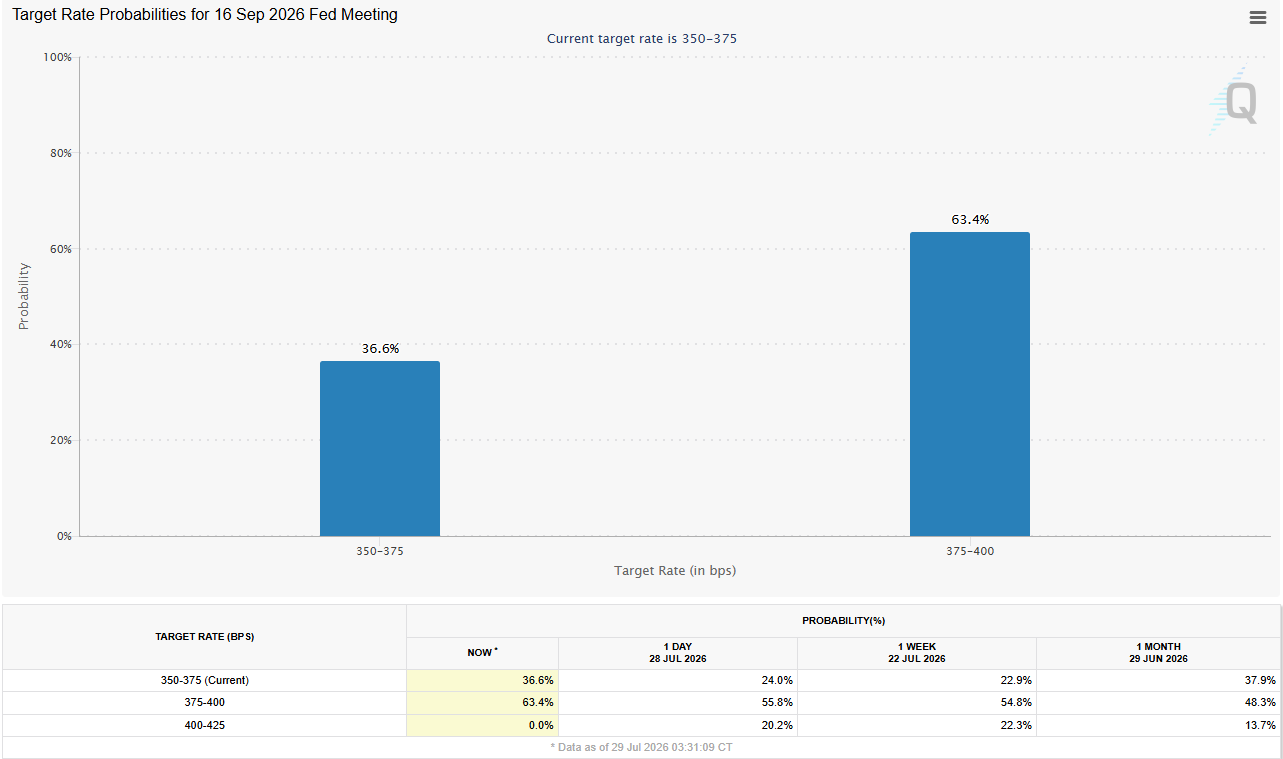

As far as market expectations go, the lack of a hike today shifted the September fed funds pricing. Odds that the Fed keeps rates unchanged at the next meeting in September rose from 24% yesterday to 37%. The 20% chance of a second rate hike that was priced in yesterday (assuming there was a hike today) was more or less split between another hold and a 25bp hike. For the rest of the year, cumulative rate hikes fell from 40bp yesterday to 33 today, back where they were a month ago.

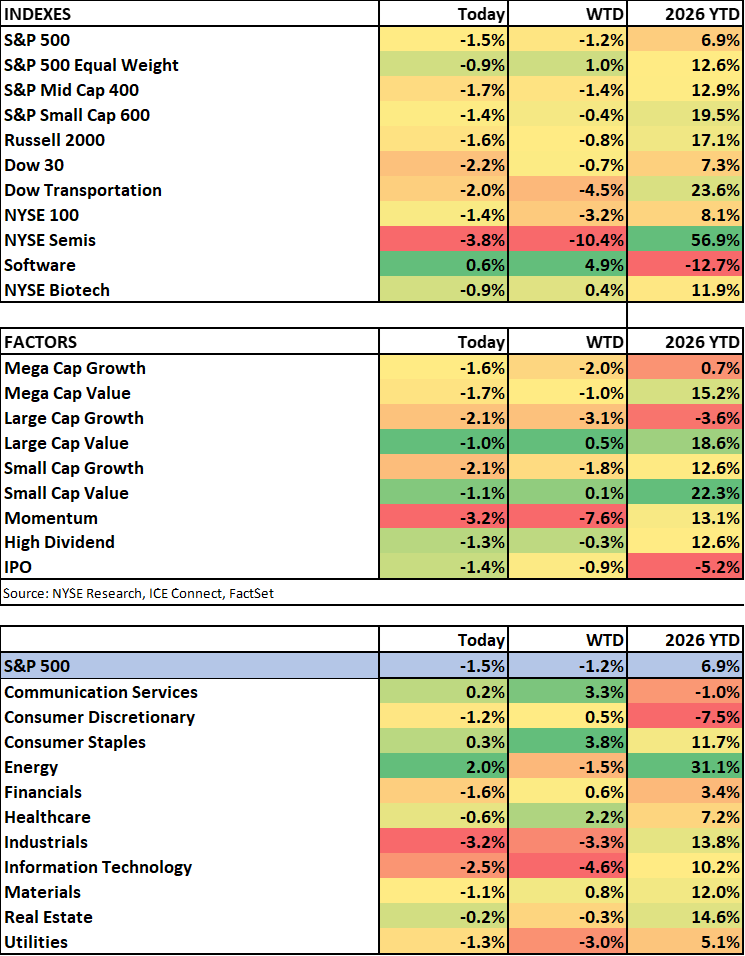

Equity markets rallied during the beginning of the press conference but failed to clear yesterday’s high (or reclaim the 50d ma) before turning sharply lower in the final hour of trade. The S&P 500 fell 130pts from the high, ending at session lows down 1.5%. The AI capex beneficiaries got hit the hardest with both the SMH/DRAM ETFs falling >5%. Software continued to hold up which may just be related to the de-grossing at hedge funds. The other sector activity was consistent with where markets were ahead of the meeting. Energy was the best performing sector for obvious reasons. The defensive bid helped consumer staples end with modest gains.

After the close the Meta missed numbers and is trading down >5%. Microsoft is trading modestly higher after strong Azure results. Looking ahead tomorrow it will continue to be busy on the earnings front. Economic data will be substantial, with PCE/GDP providing a quick and important follow-up to Warsh's commentary on the inflation flight and economic resiliency. We'll also get weekly claims, and the BoE will have a rate decision of its own.

Connect with NYSE

By submitting this form you hereby expressly grant permission to use the information included thereunder to contact you for the purposes of sending periodic updates about ICE and/or its affiliates.

Your contact information will not be used for any purpose other than that for which your consent has been given. To learn more about our privacy policy, please click here.

© 2021 Intercontinental Exchange, Inc. All rights reserved. Intercontinental Exchange and ICE are trademarks of Intercontinental Exchange, Inc. or its affiliates. For more information regarding registered trademarks see: intercontinentalexchange.com/terms-of-usea