NYSE MAC Desk

Fed Recap:

STRAIGHT FROM THE TRADING FLOOR

by Michael Reinking & Eric Criscuolo

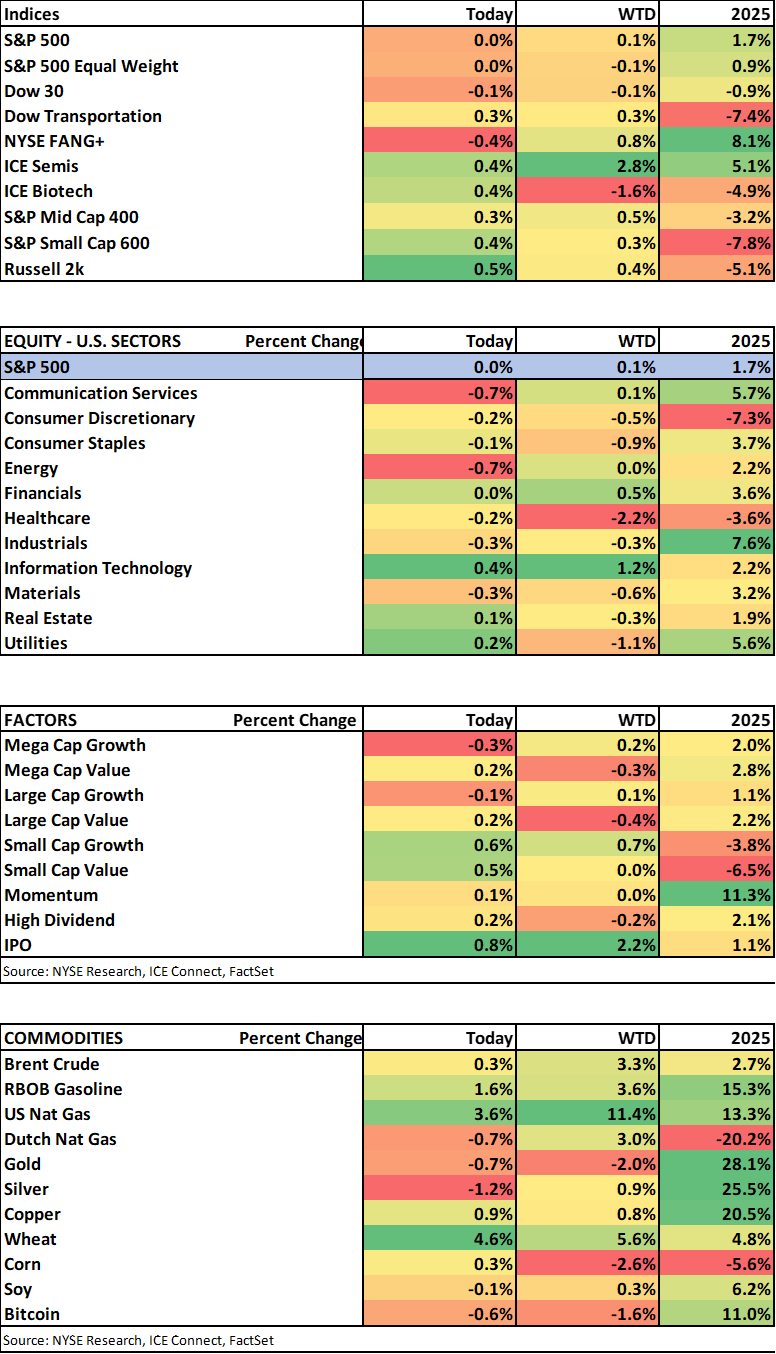

DOW 42,172 (-26), S&P 500 5,981 (+4), Russell 2000 2,124 (+24), NYSE FANG+ 14,187 (+106), ICE Brent Crude $76.18/barrel (+$1.95), Gold $3,386/oz (-$66), Bitcoin ~104.8k (-896)

- Still in wait and see mode

- Rates unchanged with a similar script

- Projections updated but do they matter?

MAC Desk Commentary:

The last FOMC meeting in May occurred a month after the reciprocal tariff pause was announced on April 9. Equities had just gone through a V-shape recovery, entering and then shooting out of a Bear market. The key messages of Chairman Powell’s press conference was the current uncertainty and need for patience, and that despite all of the recent events, the economy was in good shape. Coming into today’s meeting investors widely expected the Federal Reserve to keep rates unchanged and there were no surprises on that front. The language within the statement describing growth, employment and inflation was virtually unchanged. The only change was the suggestion that the uncertainty “has diminished but remains elevated” which the Chairman later said was a line taken directly from the Teal Book.

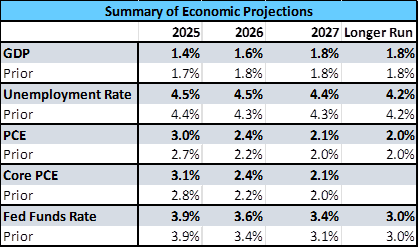

The last meeting didn’t include an update to the Fed’s Summary of Economic Projections which has not been updated since March, before Liberation Day. Directionally the revisions were in line with market expectations with GDP estimates lowered for 2025 and 2026, and a slight increase in unemployment estimates. Inflation projections also moved higher again to 3.1% in 2025 but is expected to fall pretty significantly next year to 2.4%.

Moving to the DOTS, there had been some concern that the 2025 projection for rates could shift down to 1 cut from 2 given the tight margins the last time around. That didn’t come to fruition, but the distribution clearly moved in a hawkish direction with 7 officials now projecting rates to remain unchanged through the end of the year up from 4 in March. The estimates for rates in out years also evolved in a slightly hawkish direction with only 2 additional cuts through 2027 down from 3 previously.

While we spent plenty of time slicing and dicing these projections the market response was pretty muted as the Committee would probably applaud. Chair Powell has consistently tried to downplay these projections especially in light of the amount of uncertainty in the current environment. He reiterated that view again in today’s press conference. He did address the 2025 dispersion, pointing primarily to varying economic projections leading to different outcomes, but over, and over, and over again he highlighted that the uncertainty in the forecasts does not leave anyone anchored to their forecast.

Largely, Chair Powell continued to read from the same script saying that the economy and monetary policy are in a good place which allows the Committee to be patient. The overarching message he tried to deliver was that since the economy is not deteriorating it allows the Committee to wait and see the impact of tariffs. He did acknowledge the improvement in recent inflation data, even suggesting that if it weren’t for tariffs the Fed would be in a place to cut. But he also highlighted that the Committee did not expect to see the impact from tariffs yet and it would be a couple of months before they would be ready to draw any firm conclusions. So, take a chill pill, go hit the beach, and wait until the end of the summer. But guess what? We get to do this whole song and dance again at the end of July….yay….but hopefully at that point we have some more clarity as to where tariffs end up.

On tariffs, he did talk about how the impact of tariffs gets spliced up between consumers, importers, exporters etc. and this seems to be at the heart of the matter. If ultimately tariff rates end up close to market expectations, say in the low teens, well below the levels presented in the Rose Garden, and if each of the constituents eats some portion of those tariffs then that would not lead to an inflationary loop. Once again, he also reiterated that he does not believe the labor market conditions create inflationary pressure either. Late in the press conference he did briefly address the conflict in the Middle East saying that in past episodes after energy spikes that prices tend to come down. The outlier was the 1970’s, but we are far less dependent on imported oil at this point.

In addition to the immediate actions around rate decisions, projections and statements, the FOMC continued its five-year review of the monetary policy framework. The FOMC intends to wrap up any modifications to the Statement on Longer-Run Goals and Monetary Policy Strategy by late summer. Among other things, this statement lays out the committee’s current goal of achieving inflation that averages 2 percent over time. Periods of inflation above 2% can be made up for by having periods of inflation below 2%. Before it was changed in 2020 after the last review ("perfect timing"), the previous goal was symmetric, meaning the Fed was equally concerned about inflation above and below 2%. The current statement is a bit nebulous- for one it doesn’t stipulate the time frame over which to average 2% (i.e. how long should it take to average down the screaming high post-COVID). There could be a shift back towards the prior language, or more color around the inflation timeframe, though that seems like a lot of work. After this part, discussions around enhancements to communication tools, including the SEP and dot plot, will occur in the Fall. As noted above, Powell has downplayed the dots importance, so we could eventually see some changes there.

The market reaction tells you everything you need to know. The S&P 500 traded in a less than 1% range on the day ending a touch lower than where it was when the statement was released. There was a little bit of volatility in Treasury markets but we’re only talking a couple of basis points in either direction and yields ended essentially unchanged on the day. The USD index ticked slightly higher ending up 0.1% on the day at $98.50. While this was all going on President Trump was making comments in the Oval Office which continued to show a reluctance to get more directly involved in the conflict. He is expected to meet with Israeli officials this evening. Oil ended the day around unchanged off the earlier lows while gold did pull back in the back half of the day.

Keep in mind US markets are closed tomorrow for the holiday. Before US markets reopen on Friday both the Bank of England and PBOC have rate decision. There is also a round of global inflation data. The only US economic data is the Philly Fed. Friday will be a big trading day as it is triple witch expiration, and the S&P quarterly index rebalance typically one of the heaviest volume days of the year.

Connect with NYSE

By submitting this form you hereby expressly grant permission to use the information included thereunder to contact you for the purposes of sending periodic updates about ICE and/or its affiliates.

Your contact information will not be used for any purpose other than that for which your consent has been given. To learn more about our privacy policy, please click here.

© 2021 Intercontinental Exchange, Inc. All rights reserved. Intercontinental Exchange and ICE are trademarks of Intercontinental Exchange, Inc. or its affiliates. For more information regarding registered trademarks see: intercontinentalexchange.com/terms-of-usea