STRAIGHT FROM THE TRADING FLOOR

by Michael P. Reinking, CFA - Sr. Market Strategist

Published on 8/11/26 (a/o 1:30 pm)

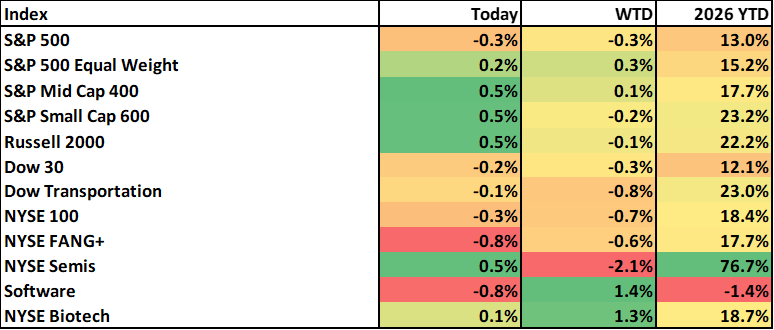

DOW 53,889 (-87), S&P 500 7,735 (-18), Russell 2000 3,032 (+14), NYSE FANG+ 18,614 (-143), ICE Brent Crude $88.89/barrel (+$1.17), Gold $4,428/oz (+$9), Bitcoin ~63.5k (-366)

- Marking time before inflation data

- Conflicting Iran headlines

- Black Leather Jackets and Patagonia Vests unite

- Check out some of the recent ICE Data/Content:

- NYSE MAC Desk Q2 Earnings Preview: rAIsing the Bar: Strong earnings, higher expectations, and the challenge of sustaining momentum

- Inside the ICE House

- James Rutledge Shares Six Decades of History Inside the NYSE

- ETF Central: Baron Capital Head of ETF Solutions Matt Camuso

- NYSE Research Insights: Behind the Record Volumes: A Hidden Opportunity

- ICE Mortgage Monitor: Mortgage Holder Equity Climbs to Record $18 Trillion as Annual Home Price Growth Reaches 14-Month High

- Market Storylines

MAC Desk Commentary:

We’re clearly in the Dog Days of Summer. Yesterday major US indices ended modestly lower in a rather subdued start to the week. Since the middle of last week markets have been trading in a pretty tight range consolidating the recent gains. Oil prices and yields moved higher yesterday which weighed on small caps and yield oriented sectors while the energy sector rebounded sharply recouping all of last week’s losses. Capital intensity of the AI Capex boom was once again in focus with Intel announcing a $15B equity raise and the FT reporting that Nvidia was working with major Wall Street firms to provide financing of up to $500B for data centers.

After the close Nvidia announced it is partnering with Apollo Group, Blackstone, BlackRock, Brookfield Asset Management, Goldman Sachs and KKR to establish a “compute financing platform” with Nvidia having the option to backstop 25% of the $500B. The stocks of all partners involved are trading higher and this is also helping stocks across the AI infrastructure complex and private credit. However, the hyperscalers (ex-Meta) are all under pressure as this signals more spending and competition going forward. It also highlights the fact that financing is a choke point, even Nvidia's balance sheet has its limits. Speaking of funding, the WSJ is reporting that Anthropic is now targeting a potential IPO in the fall ahead of midterms. Intel also upsized its equity offering to $20B highlighting that there is still demand out there. It is amazing how perception has changed and now $5B just sounds like a spit in the bucket.

Conflicting Middle East headlines continue to swirl about the state of negotiations and the US fired on a Panama-flagged ship trying to cross the blockade. Oil prices are modestly higher holding onto yesterday’s rally but did pullback from the overnight high after a reports that Pakistan’s interior minister is in Tehran. Treasury yields were also higher overnight but pulled back modestly. The trading action at the index level remains pretty tame as we await tomorrow’s inflation data. The S&P 500 is trading slightly lower with the mega-cap tech stocks a drag. The equal weight and small cap indices are recouping some of yesterday’s losses. As we head to print, the S&P 500 is down 19pts to 7,734 (-0.2%), the Dow is down 89pts to 53,887 (-0.2%), while the Russell 2k is up 14pts to 3,032 (+0.5%).

A little busier in terms of economic data but it is not having much impact on trading. The NFIB small business index rose from 97.4 last month to 99.8, its best level since last August. The report noted a jump in owners expecting to hire- a net 20% of owners plan to create new jobs over the next 3 months, up from 11% last month. That diverges from the continued downtrend in the ADP weekly employment data, which showed a further drop today to 8.25K/week, down from 15.0K in the prior report and the sixth straight decline overall. The ADP number also comes after last week’s surprise negative monthly jobs report. Existing home sales was about in line with estimate but remained at depressed levels.

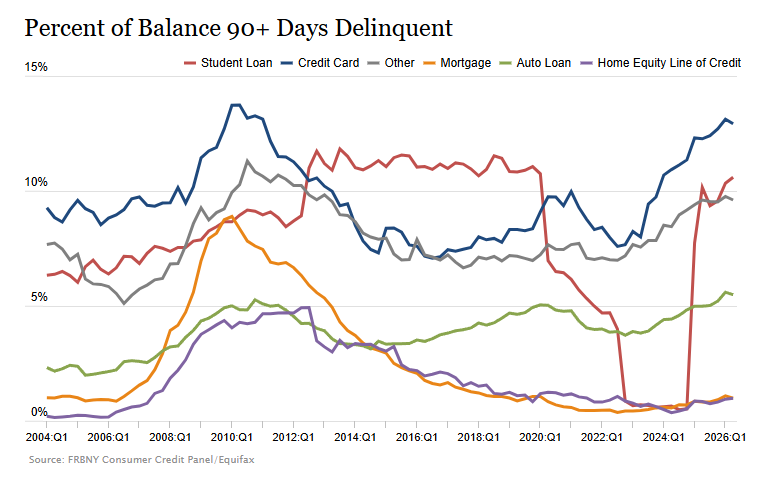

The NY Fed released its Quarter Report on Household Debt and Credit which a slight decrease in household debt (-0.1%) to $18.8T driven by a decline in mortgage balances while most other categories increased. There was also a slight improvement in delinquencies with 4.7% of outstanding debt in some state of delinquency down 0.1% from the previous quarter. Credit card and auto delinquencies >90 days remain elevated.

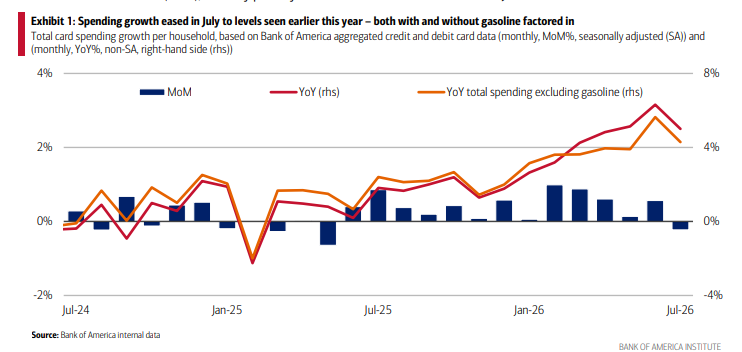

Ahead of Friday’s retail sales Bank of America Institute noted that consumer spending growth moderated to 5% y/y from 6.3% in June but suggested that this was related to one-time items like the pull forward of Prime Day and unwinding World Cup spending.

Treasury yields are down ~3bps across the curve. There was a 3yr auction at 1:00 which was well received pricing through the when issued market while other underlying metrics were also strong. All eyes now turn to tomorrow’s CPI report and there is also a 10yr auction tomorrow afternoon.

- US 2yr -3bps to 4.22%, 5yr -2bps to 4.39%, 10yr -2bps to 4.69%, 30yr -2bps to 5.24%

- USD index: +$0.06 to $99.76

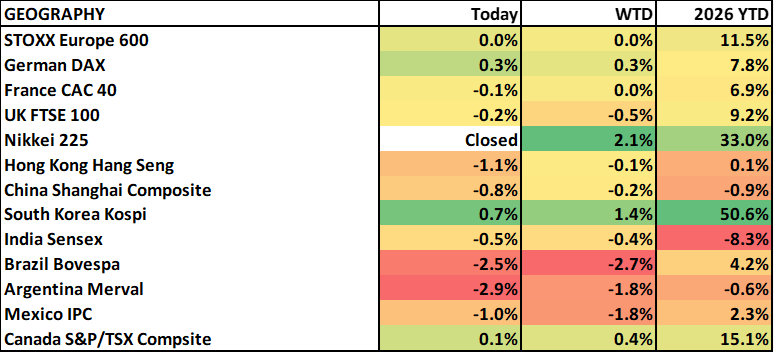

Japan was closed overnight while China’s markets were lower with the Hang Seng lagging and Internet companies soft (Tencent, Baidu -2%). Robotics company Unitree’s upcoming IPO was apparently over 8,000 times oversubscribed by retail investors. The Hang Seng Tech Index will expand from 30 to 50 stocks in December, according to an index consultation paper, adding more AI and robotics stocks and younger tech companies, attempting to more fully capture the (hopefully) early gains of those companies. Australia’s central bank left its policy rate unchanged, as expected and took down inflation expectations. The Australia ASX finished modestly higher with miners and oil/gas mostly higher (Newmont +3%, Woodside +4%). Europe closed around unchanged with oil and gas stocks leading while insurance, food/beverage/travel lag.

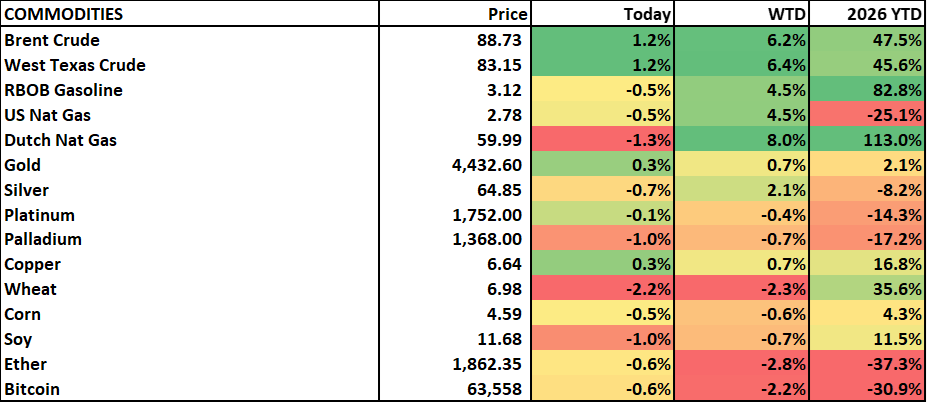

Oil prices are up ~1% but off the overnight high. Natural gas prices are pulling back modestly giving back some of yesterday’s gains. Metals are mixed. Gold nearly tagged its 200d overnight trading just under 4,500 before giving up about half its gains. Ag is lower. Crypto has given up overnight gains trading slightly lower. The SEC announced that it would be holding an open meeting on Friday to “consider whether to issue a release proposing new rules to create a tailored offering regime for certain investment contracts involving crypto assets.” This is a procedural step in the rulemaking process which typically takes 12 - 18 months.

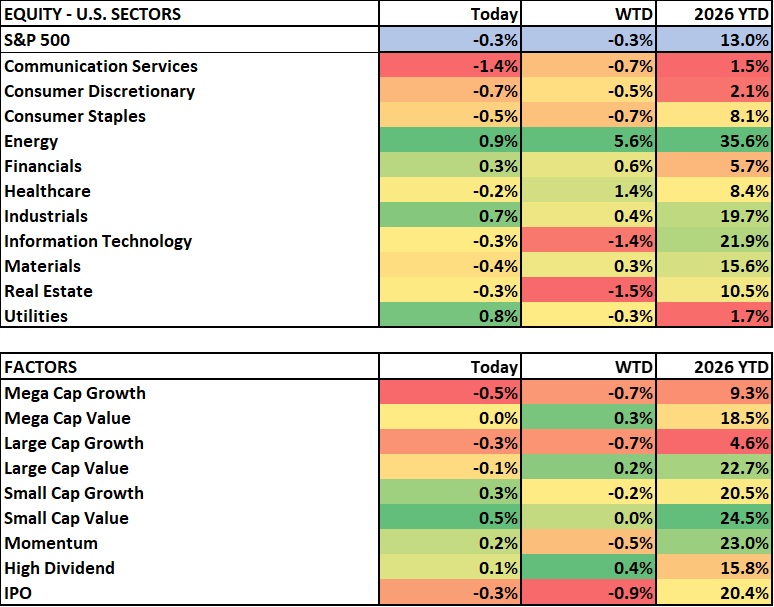

Withing the S&P 500 only 4 of 11 sectors are trading higher though breadth is slightly better than 1:1 adv:dec. Energy is leading to the upside. Industrials are being helped by AI infrastructure, airlines and building products companies. Utilities are broadly trading higher with the pullback in yields though IPPs are some of the best performing. Asset managers are the best performing stocks with financials. Hyperscaler weakness is dragging down comm services, consumer discretionary and info tech. Within consumer discretionary housing, autos and travel related stocks are trading higher. Apparel and footwear after disappointing On Holding results. Within tech Nvidia has turned slightly lower while the other direct chip competitors (AMD/AVGO) are under a bit of pressure as this strengthens their ecosystem. Software is underperforming giving back some of the recent gains.

Looking ahead to tomorrow CPI is the main event. On the earnings front there are a couple of tech reports that will get some attention. As well as a couple of restaurants including CAVA which is on the menu for the MAC Desk lunch today.

Earnings:

After-Market: CAVA, CRWV, FLY, HRB, LITE, QNT, SMCI

Pre-Market: AMCR, EAT, EYE, KTB, NBIS, PFGC, SLAB, TORO, WRD

After-Market: AOSL, BTGO, CAE, CBRS, COHR, CSCO, DOX, ENS, EQPT, GO, HLIT, INFQ, JACK, NNE, PAR, REZI, SECZ, SPCE, STAA

Economic Data:

US:

- NFIB business sentiment: 99.8 vs 97.5 cons, prior 97.4

- ADP weekly payrolls: 8.25K vs prior 15.0K

- Existing Home Sales: 4.06 vs. 4.07ml cons., prior revised to 4.13ml from 4.09ml

Global:

- RBA rate decision: Unchanged as expected (4.35%)

STRAIGHT FROM THE TRADING FLOOR

by Eric Criscuolo - Market Strategist

Published on 8/11/26 (a/o 9:00 am)

Good morning,

Equity futures are slightly higher this morning, following a rather subdued start to the week yesterday. Feels like we’re in the Dog Days of summer and are drifting into the CPI report on Wednesday. S&P futures are just off their overnight highs, ticking lower after news that US forces fired on a Panama-flagged ship that tried to run the Iran blockade. That came after reports that negotiations between Oman and Iran on the Strait are in advanced stages, and also that Pakistan’s interior minister is in Tehran for talks.

On the earnings front, stock reactions are leaning negative. Getty Images (GETY, “continued pressure in Agency and iStock e-commerce”), Upwork (UPWK, navigating AI transition and continued pressure in SEO), On (ONON, revenue miss, guidance lowered) and Tencent Music (TME) are all trading down over 10%. On the upside, Babcock & Wilcox (BW) is trading up over 30% on strong demand for its boilers and energy solutions in data center builds. Plug Power (PLUG) and Rackspace (RXT) are up ~10%. In other news, Morgan Stanley announced a $1.5 trillion program to finance US infrastructure projects and strategic initiatives, which sounds similar to a program from JP Morgan.

Treasury yields were modestly higher before the Pakistan report sent yields and oil lower. Yields are currently down 1-2bp. The US Dollar Index is a bit higher. It’s another quiet day on the eco calendar. The NFIB small business index rose from 97.4 last month to 99.8, its best level since last August. The report noted a jump in owners expecting to hire- a net 20% of owners plan to create new jobs over the next 3 months, up from 11% last month. That diverges from the continued downtrend in the ADP weekly employment data, which showed a further drop today to 8.25K/week, down from 15.0K in the prior report and the sixth straight decline overall. The ADP number also comes after last week’s surprise negative monthly jobs report. Towards the end of yesterday’s session Cleveland Fed President and member of The Dissenters, Beth Hammack, discussed her outlook. She said a single 25bp hike was insufficient to impact current inflation, and current rates aren’t restrictive enough to slow growth. She also distanced herself from the “let the market do the Fed’s work” narrative by saying the Fed must be proactive and not rely on market movements.

Crude is well off its highs and turned negative after the news of the Iran negotiations. US nat gas is slightly higher following yesterday’s gain, while European gas gives back some of its sharp gains yesterday. Gold is up ~1%, pulling into the 100d ma level ~$4430. Ag is mostly lower while Bitcoin and Ether are modestly higher.

Earnings:

After-Market: AAON, ACHR, ACM, ALC, AMTM, ASTS, BW, BZH, BBIO, GETY, HIMS, PLUG, QUBT, RKLB, SPG, UPWK

Pre-Market: ARMK, CAH, MIDD, ONON, RXT, SFD, TME. VG, VSTS

After-Market: CAVA, CRWV, FLY, HRB, LITE, QNT, SMCI

Economic Data:

US:

Equity futures are slightly higher this morning, following a rather subdued start to the week yesterday. Feels like we’re in the Dog Days of summer and are drifting into the CPI report on Wednesday. S&P futures are just off their overnight highs, ticking lower after news that US forces fired on a Panama-flagged ship that tried to run the Iran blockade. That came after reports that negotiations between Oman and Iran on the Strait are in advanced stages, and also that Pakistan’s interior minister is in Tehran for talks.

On the earnings front, stock reactions are leaning negative. Getty Images (GETY, “continued pressure in Agency and iStock e-commerce”), Upwork (UPWK, navigating AI transition and continued pressure in SEO), On (ONON, revenue miss, guidance lowered) and Tencent Music (TME) are all trading down over 10%. On the upside, Babcock & Wilcox (BW) is trading up over 30% on strong demand for its boilers and energy solutions in data center builds. Plug Power (PLUG) and Rackspace (RXT) are up ~10%. In other news, Morgan Stanley announced a $1.5 trillion program to finance US infrastructure projects and strategic initiatives, which sounds similar to a program from JP Morgan.

Treasury yields were modestly higher before the Pakistan report sent yields and oil lower. Yields are currently down 1-2bp. The US Dollar Index is a bit higher. It’s another quiet day on the eco calendar. The NFIB small business index rose from 97.4 last month to 99.8, its best level since last August. The report noted a jump in owners expecting to hire- a net 20% of owners plan to create new jobs over the next 3 months, up from 11% last month. That diverges from the continued downtrend in the ADP weekly employment data, which showed a further drop today to 8.25K/week, down from 15.0K in the prior report and the sixth straight decline overall. The ADP number also comes after last week’s surprise negative monthly jobs report. Towards the end of yesterday’s session Cleveland Fed President and member of The Dissenters, Beth Hammack, discussed her outlook. She said a single 25bp hike was insufficient to impact current inflation, and current rates aren’t restrictive enough to slow growth. She also distanced herself from the “let the market do the Fed’s work” narrative by saying the Fed must be proactive and not rely on market movements.

- US 2yr -2bps to 4.23%, 5yr -2bps to 4.40%, 10yr -2bps to 4.69%, 30yr -1bps to 5.24%

- USD index: +$0.01 to $99.72

Crude is well off its highs and turned negative after the news of the Iran negotiations. US nat gas is slightly higher following yesterday’s gain, while European gas gives back some of its sharp gains yesterday. Gold is up ~1%, pulling into the 100d ma level ~$4430. Ag is mostly lower while Bitcoin and Ether are modestly higher.

Earnings:

After-Market: AAON, ACHR, ACM, ALC, AMTM, ASTS, BW, BZH, BBIO, GETY, HIMS, PLUG, QUBT, RKLB, SPG, UPWK

Pre-Market: ARMK, CAH, MIDD, ONON, RXT, SFD, TME. VG, VSTS

After-Market: CAVA, CRWV, FLY, HRB, LITE, QNT, SMCI

Economic Data:

US:

- NFIB business sentiment: 99.8 vs 97.5 cons, prior 97.4

- ADP weekly payrolls: 8.25K vs prior 15.0K

- 10:00am Existing Home Sales

- 11:00am Household Debt

- 1:00pm 3y auction

- 4:30pm API Crude inventories

- RBA rate decision: Unchanged as expected (4.35%)

By submitting this form you hereby expressly grant permission to use the information included thereunder to contact you for the purposes of sending periodic updates about ICE and/or its affiliates. Certain indices mentioned above are administered by ICE Data Indices, LLC.

Your contact information will not be used for any purpose other than that for which your consent has been given. To learn more about our privacy policy, please click here.

© 2025 Intercontinental Exchange, Inc. All rights reserved. Intercontinental Exchange and ICE are trademarks of Intercontinental Exchange, Inc. or its affiliates. For more information regarding registered trademarks, limitations, restrictions, and other important information, please visit intercontinentalexchange.com/terms-of-use.