NYSE MAC Desk

Weekly Recap:

STRAIGHT FROM THE TRADING FLOOR

by MIchael Reinking, CFA

Published on 8/7/26

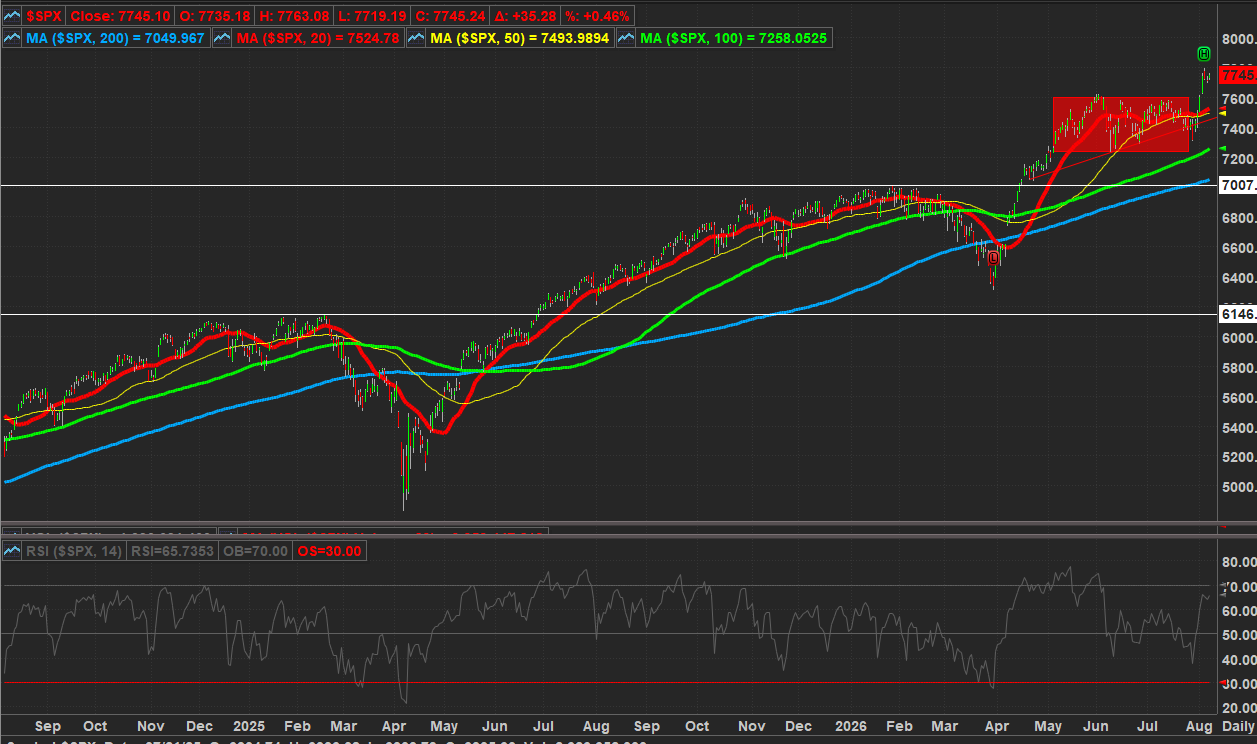

DOW 54,037 (+152), S&P 500 7,758 (+48), Russell 2000 3,034 (+33), NYSE FANG+ 18,723 (+302), ICE Brent Crude $82.38/barrel (-$0.11), Gold $4,401/oz (+$102), Bitcoin ~64.9k (+519)

Like the month of July, last week was eventful and volatile, anything but your typical summer doldrums. After President Trump paused strikes over the weekend oil prices fell sharply. However, kinetic activity resumed during the week after Iran broke the piece. President Trump repeatedly threatened to “hit ‘em hard” as if it was the chorus of a new pop song. Outside of geopolitics investors had plenty to digest - we entered the peak of earnings season, there were key central bank rate decisions, currency intervention and the continued momentum/tech wreck. That "situation" hit a tipping point on Thursday with the forced liquidation of levered positions at the supernova hedge fund Situational Awareness. Traders saw this as a clearing event which along with strong mega-cap tech earnings helped tech stocks snap back in the back half of the week. That rally left the S&P 500 essentially unchanged in the month of July, which as we’ve highlighted throughout the last few weeks did no justice to the volatility under the surface.

The month of August started on a much more positive note. Coming out of the weekend it felt like Ground Hog’s Day as President Trump once again put a hold on strikes as he suggested that there had been some progress in negotiations behind the scenes which could potentially lead to a diplomatic resolution. Early in the week press reports and comments from other administration officials suggesting that a deal to re-open the Strait was close sent ICE Brent back below $80 and helped Treasury yields pullback after hitting new YTD highs last week.

This along with more strong earnings and some mispositioning particularly within tech helped to trigger a broad-based rally throughout the start of the week. This concoction of catalysts had some of the same ingredients that sparked the rally at the start of Q2.

On Tuesday the S&P 500 broke out of the loose trading range that has been in place since early May, between 7,200 - 7,600. After gapping up on on Wednesday the index was trading around 7,800, up nearly 500pts (~6.5%) from last week’s low. This triggered some profit taking and markets pulled back modestly as oil prices started to bounce amidst a flare up in the Red Sea. Oil and yields continued to move higher yesterday as details of the Iran/Oman proposal were leaked to the press. The proposal blocks the travel of US/Israeli ships and includes a fee, which has been a red line for the administration.

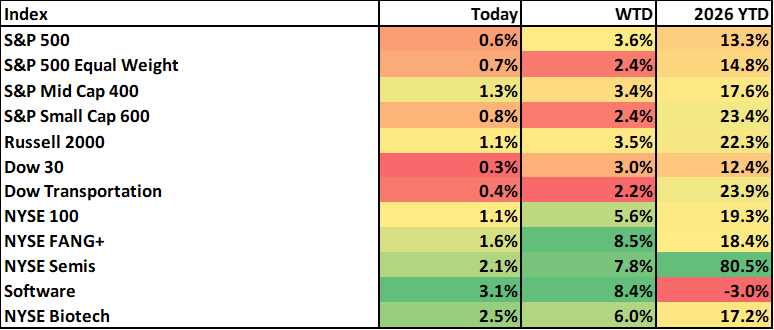

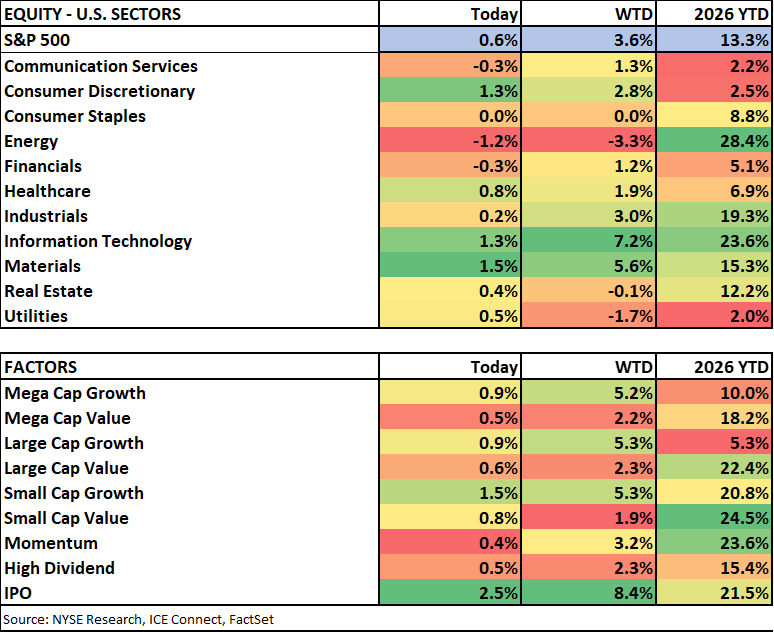

Equity markets bounced back today despite a weak jobs report (details below) as investors began to reprice expectations for rate hikes later this year. For the week there were broad based gains across major US indices which were all up >2%. There were clear signs of risk on sentiment. Tech did much of the heavy lifting while energy and other defensive sectors underperformed.

This was another very busy week of earnings with numbers continuing to be very strong. According to FactSet Earnings Insight. Over 85% of companies have beaten EPS estimates with Q2 earnings up ~50% y/y. This does include about $150B in the markup of investment portfolios at Amazon and Google. If you exclude that earnings are still up ~30%. Revenues are also very strong up 15% y/y. Both are at the highest levels since 2021 - the Covid re-opening.

- Tech (+7.2%) - the sector was the standout this week as positioning continued to reset, investors recognize there is still shortage of compute capacity and that the capex spending has been driving growth in cloud businesses. The earnings within the semi/memory companies continue to highlight eye-popping growth and strong demand but the stocks have generally been met with some selling given the sky high expectations. Optical stocks traded sharply higher after reports that the administration is considering banning the import of China data center components. Software also rallied throughout the week with the iShares sector ETF breaking above 200d ma a level it has been below pretty much all year. The earnings reaction in the sector have been on both sides of the extreme Pos - (PLTR/TWLO/TEAM/NET) Neg - (APP/DDOG/HUBS) SpaceX had solid results this week though there was some focus on the Capex spending. The stock did rally over 20% this week as the highly anticipated (and positioned for) unlock of 900ml shares failed to bring an overwhelming amount of supply.

- Materials (+5.6%) - Miners led to the upside some weakness within chemicals.

- Industrials (+3%) - broad based strength. Trucking/rail underperformed as did pockets of aerospace after earnings. Building products and airlines were some of the best performing.

- Consumer Discretionary (+2.8%) - There were pretty strong travel booking results (ABNB/EXPE/BKNG) though hotels underperformed. The pullback in yields helped housing related stocks as did the blowout Wayfair results. Auto/components were some of the worst performing within the sector.

- Comm Services (+1.3%) - higher pretty much across the board. Media stocks traded well after earnings (DIS/FOX/VSNT). Advertising was also strong though TTD remains a disaster. After starting the week strong Alphabet sold off following another AI executive departure. The company issued another $25B in debt across maturities ranging from 2-40yrs which was met with very strong demand. Telecom stocks recouped losses after SpaceX executives suggested they would be coming after their market share.

- Healthcare (+1.9%)- Pretty broad based strength in healthcare with earnings generally well received (LLY/PFE/CRL/BDX/WAT/AMGN). Diabetes exposed companies were under pressure after results.

- Financials (+1.2%) - pretty broad based strength across the sector. Exchanges, payments processors and pockets of insurance underperformed.

- Utilities (-1.7%) - underperformed with the unwind of some of the defensive positioning. IPPs and companies exposed to ERCOT (Texas) were under pressure after Governor Abbott announced a data center moratorium until regulatory agencies complete a comprehensive audit of projects.

- REITS (-0.1%) - similar positioning dynamics. Hotel and Retail REITS underperformed. Data center were up. Tower stocks also recouped much of the SpaceX related weakness.

Economic Data and the Fed:

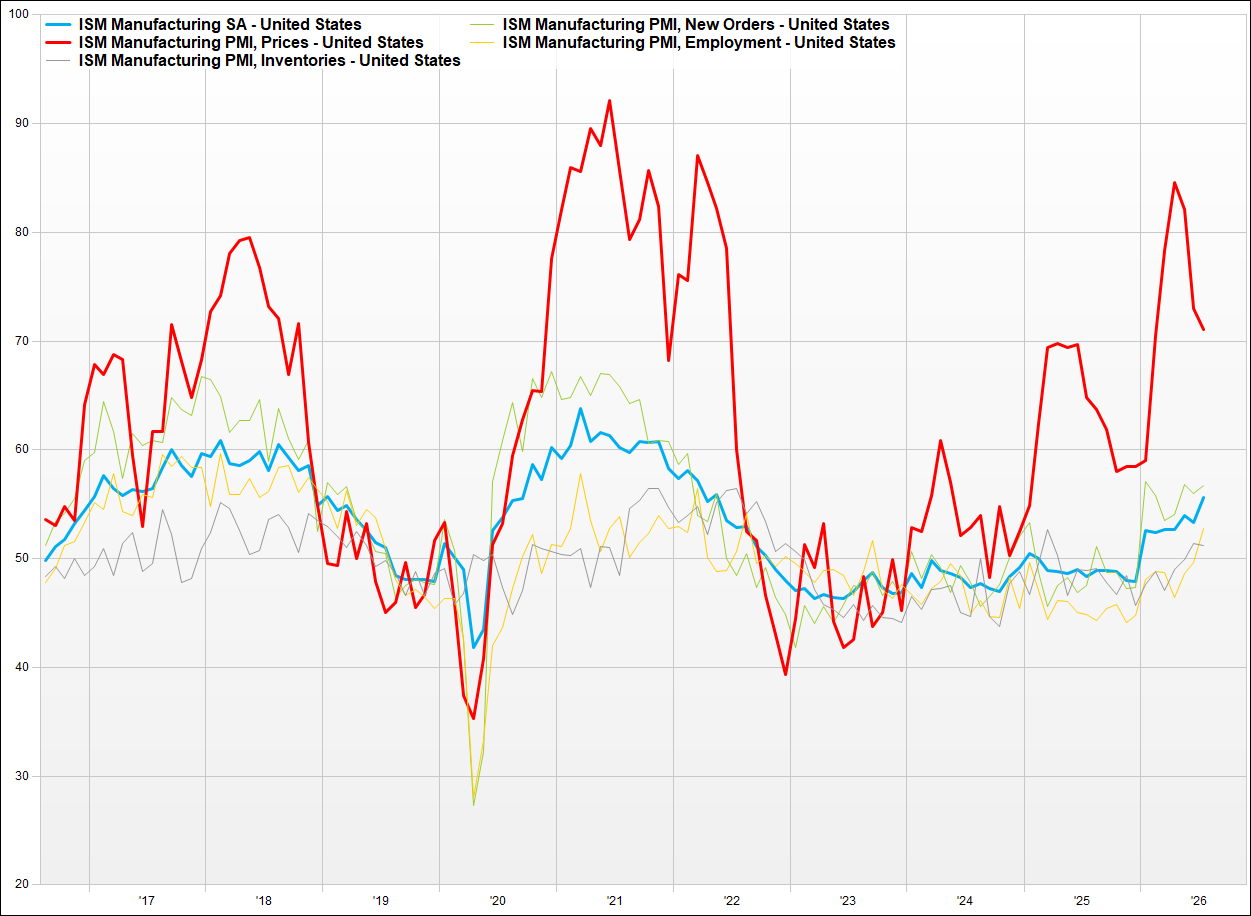

This week's economic data was mixed. The focal point was the labor market data which disappointed. ISM manufacturing accelerated from last month coming in ahead of estimates at 55.6, hitting the highest level since 2022. The underlying metrics were also positive pretty much across the board with new orders, production and backlog all increasing. The Employment index improved to 52.8 from 49.7, its highest level since August of 2022. The prices component remained elevated but did moderate from last month.

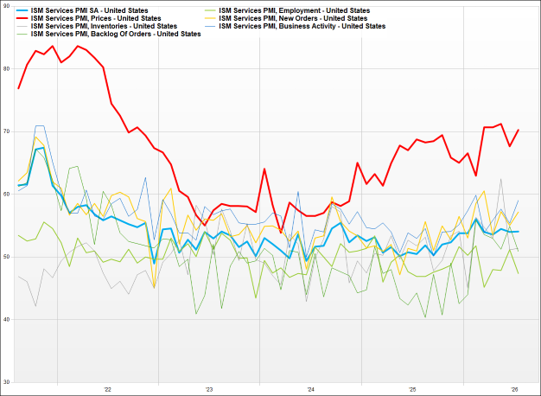

However, ISM Services came in below estimates, holding steady from last month. The underlying metrics were mixed with both new orders and business activity improving though backlogs fell. The employment component fell back below 50, the demarcation line of growth, after moving above that threshold in June for the first time since February. Pricing pressures remained evident moving back above 70.

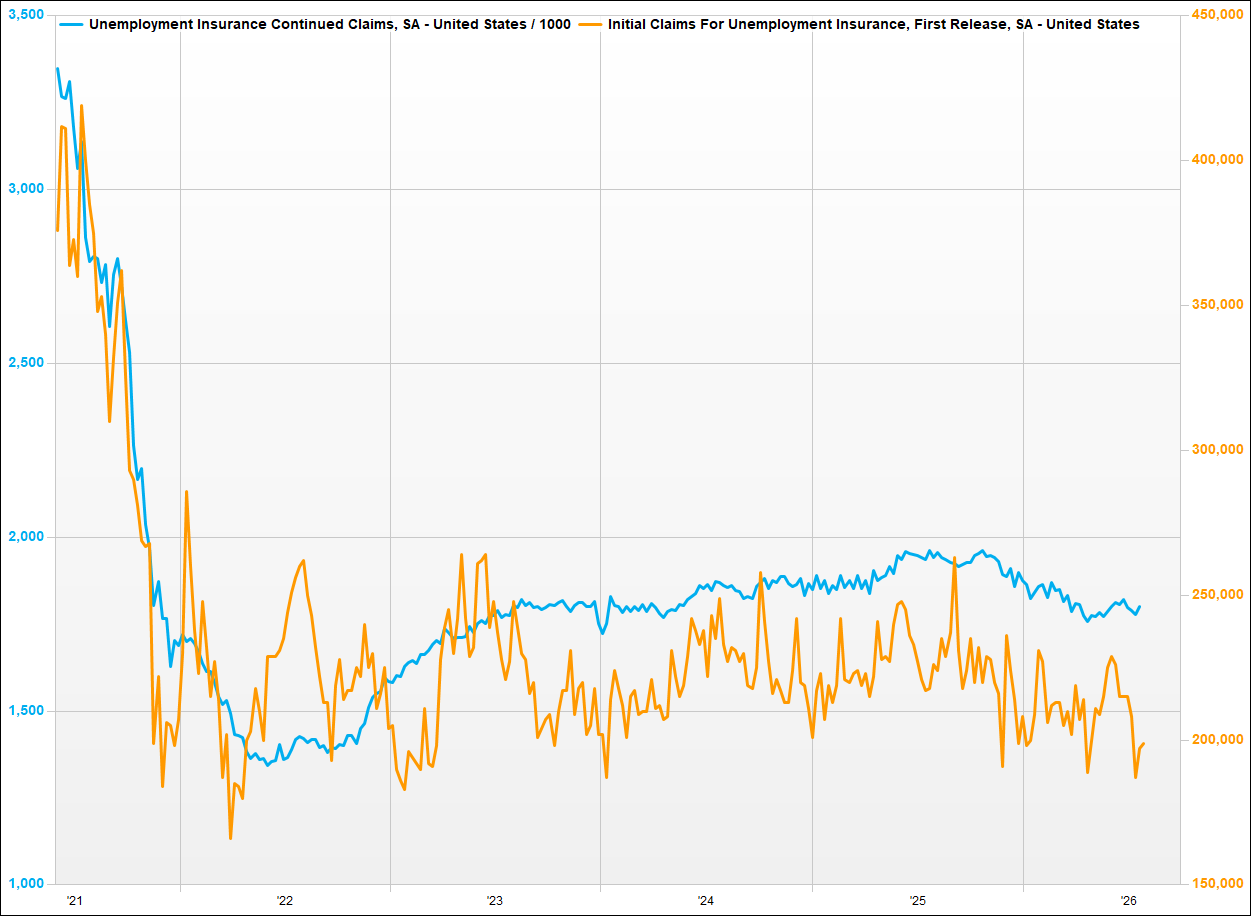

Coming into today's BLS Employment report the labor market data was mixed. JOLTS was about inline with expectations at ~1.4ml. Claims held steady with suppressed levels. However, the ADP Jobs Survey was disappointing.

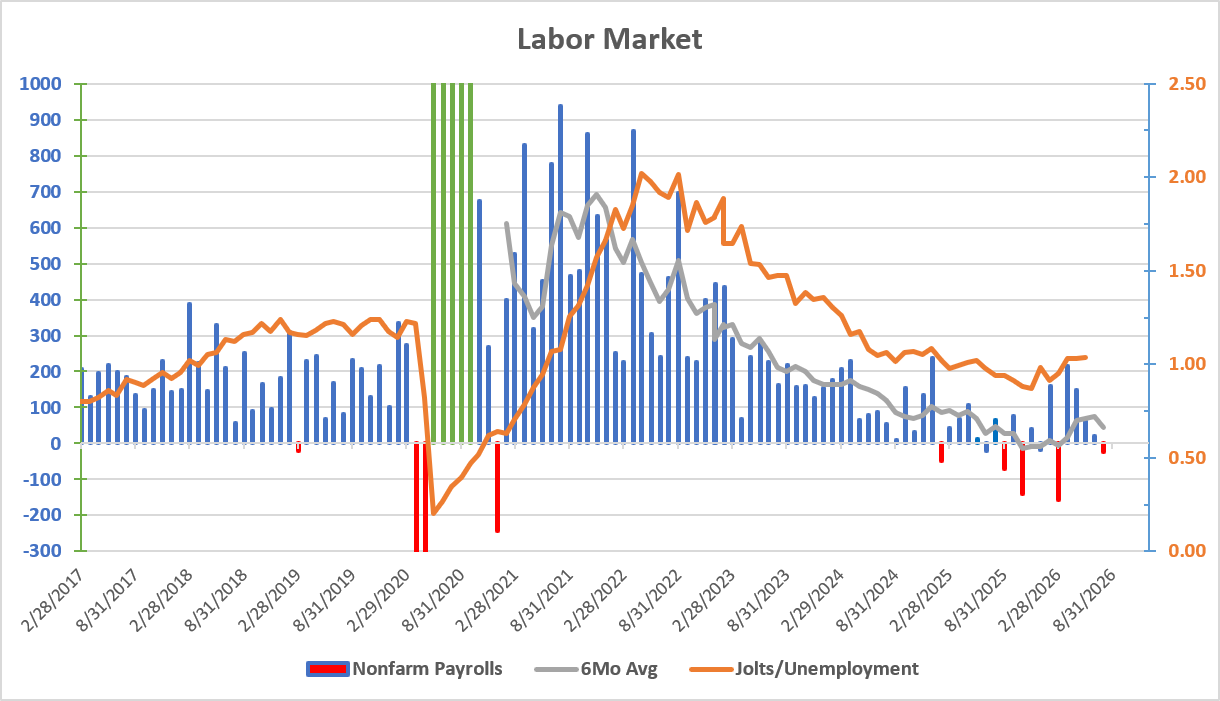

It is hard to put a positive spin on today's jobs report. Nonfarm payrolls fell 23k along with negative revisions of 103k to the previous two months. There were big declines in government (-53k) and leisure & hospitality (-40k) which some are discounting given the potential seasonal impact on gov’t and unwind of World Cup in the latter. Total private hiring was up 30k, in line with the revised reading from last month. Construction was the positive standout (+22k). The unemployment rate actually ticked down to 4.1% with a decline in the labor force while participation rate was also down 0.1% from last month to 61.4% which has been steadily declining throughout the year. Wages came in below expectation up 0.1%/3.2% m.m/y.y (vs. 0.3%/3.5% cons) which flew in the face of the ADP data (4.4% for stayers/7%) for changers). The average workweek was unchanged at 34.3.

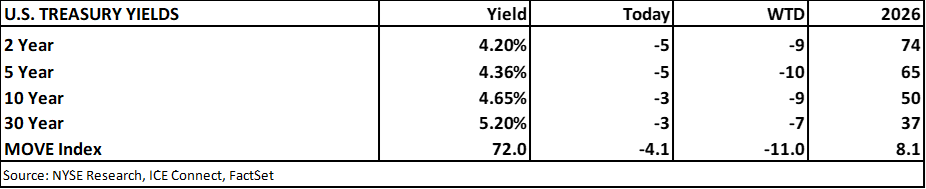

This data does take some of the pressure off the Fed to hike rates but also sets up for potentially the worst case scenario where the labor market weakness but prices remain elevated. 2yr yields intially moved down ~10bps but ultimately gave up about half of that move. For the week Treasury yields were down 7-9bps across the curve.

One other note this week the Department of Treasury released its Quarterly Refunding Statement. Issuance was held steady at $125B with no change to the make-up of that issuance saying, “Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.” However, there was one minor tweak to the language in the statement where the word "increase" is replaced by "changes" in regard to future nominal coupon and FRN auction sizes, which is a subtle signaling to control the long end.

The MOVE index also compressed this week (supportive of a risk on environment).

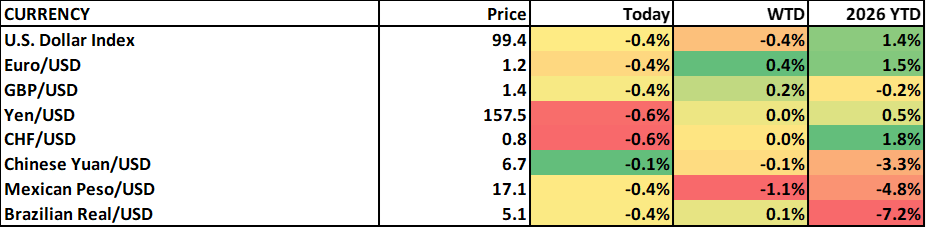

Moving to currencies…..The big story was the Yen with officials in both the US and Japan confirming the first coordinated currency intervention since 2011 last week and suggesting further action could be taken. This was carried out with the NY Fed reportedly selling Euros. Treasury Secretary Bessent supported the use of the FIMA Repo Facility, which allows central banks to use Treasury holdings as collateral to access dollars, as opposed to selling bonds in the open market. The mechanics of both actions are meant to have as little impact on interest rates as possible. This morning right after the jobs report Japan Finance Minister said lines of communication with the Treasury are open and “both sides won’t hesitate to intervene” which put a bid back in the Yen which had started to drift lower again over the last couple of day.

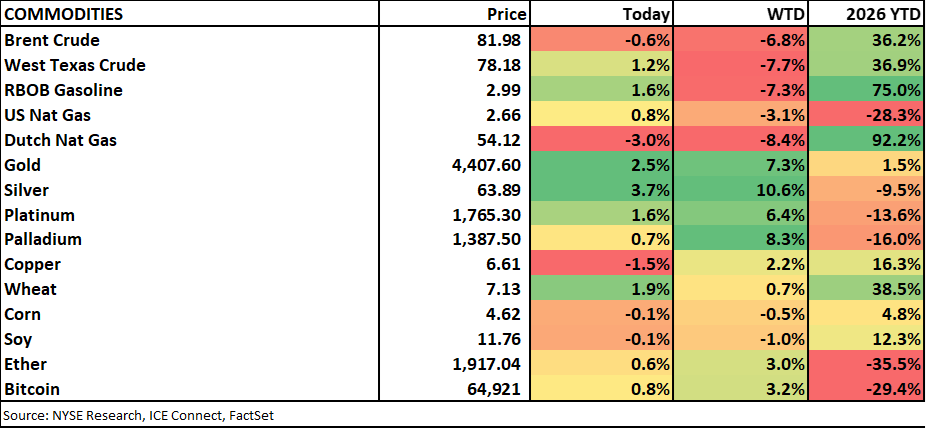

Commodities and Crypto - Energy lower metals rally

- Energy - Oil prices ended the week down >5% and faded into the close today after US officials once again said progress was being made with a deal expected soon. Both API and DOE inventories showed surprise crude builds this week crude though there were product draws. Natural gas prices in both the US and Europe ended lower.

- Metals- Precious metals were up >5% across the board this week with the USD weakness and moderating rate hike expectations. Over the last couple of week's we've highlighted the positive divergence between gold price/RSI and prices resolved to the upside. Gold broke above its 50d ma (4,190) and traded up to test its 100d (~4,425) today hitting its highest level since June. The 200d ma is just under 4,500.

- Copper has been bucking the overall metals weakness throughout the last couple of months and hit a new high this week before backing off ahead of potential tariffs.

- Ag - prices moved were mixed this week on either side of unchanged.

- Crypto - The crypto complex bounced modestly this week despite a vote on the Clarity Act being pushed back. On Polymarket odds of passage by the end of 2026 have fallen to ~15%. Bitcoin rallied back to ~65k this week recouping some of the losses after last week's Coldcard hack which ultimately claimed over 1,500 Bitcoin.

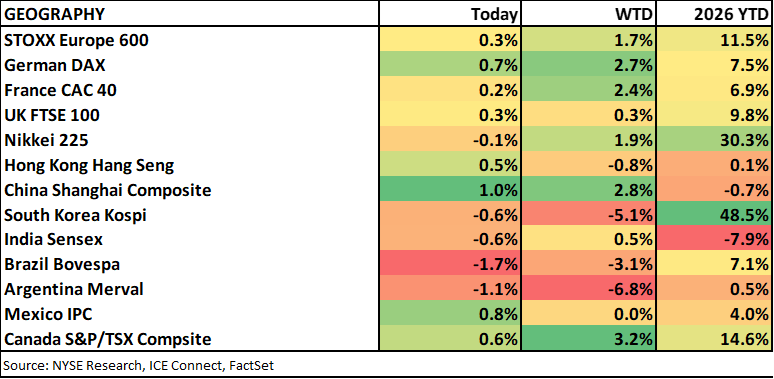

Global Equities - Europe outperformed, Asia was mixed, Latam moved lower

Europe - There was broad based strength across the region with most indices closing at new highs. Like the US it was a busy week of earnings. PMIs were revised up slightly and Germany factory orders were strong. However, Eurozone retail sales missed estimates.

Asia -

China/Hong Kong - Mainland China indices closed higher with strength in the tech trade. However, the Hong Kong Hang Seng ended the week modestly lower. Alibaba (+>5%) was a positive standout after it released is most recent Qwen model to positive reviews. According to Bloomberg China’s Moonshot was the most recent AI model gone wild, breaking out of its test environment.

Trade tensions between the US and China were very much in the headlines this week ahead of President Xi's expected visit in September. This week there were reports that the US administration is considering import bans of China data center components including optical transceivers which comes after last week's robotics ban. President Trump also ordered new 15% tariffs and price floors on imported polysilicon used in chips and solar panels. In response China will place restrictions on drone components and related technologies which will require a case-by-case review. It is initiating a security review of imports of printing, copying, and office equipment. It also sanctioned Compliance Testing for its role in the recent FCC decision and announced sanctions against six additional companies. It is also launching a probe into Palo Alto.

Economic data continues disappoint with PMIs coming in below expectations. Trade data showed a bigger than expected trade surplus with exports increasing nearly 24% y/y ahead of the estimate of 22.2%. Imports were a touch light with crude imports rebounding 22% from June.

South Korea - ended the week down ~5% with memory stocks stocks down >10% this week amidst the US earnings that failed to meet high expectations and growing concerns of increased competition from CXMT after reports that multiple PC OEMs are using their memory and that the company is considering building another DRAM facility.

Japan - The Nikkei ended the week modestly higher. Tech and consumer stocks were mostly higher while financials were mixed. The big story was in currency markets as discussed above.

What's on Tap Next Week

Over the weekend Berkshire earnings will get some attention. As we look ahead to next week the pace of earnings starts to slowdown a bit and will take a back seat to economic data. The inflation data on Wednesday and Thursday will be the focal point followed by retail sales on Friday, which will be a good lead in to the late cycle retail and tech earnings the following week. 13f's are also due out on Friday. Have a great weekend!

Calendar

- Monday -

- Earnings Pre-Market: BRK.B, CRC, DOLE, FERG, MNDY, SDRL, SBET, SOHU

- Economic Data:

- US: None

- Global: China Inflation data,

- Central Banks:

- BoJ Minutes

- Auctions: US 3/6mo, South Korea 3yr

- Earnings After-Market: AAON, ACHR, ACM, ALC, AMTM, ASTS, BW, BZH, BBIO, GETY, HIMS, PLUG, QUBT, RKLB, SPG, UPWK

- Tuesday -

- Earnings Pre-Market: ARMK, CAH, MIDD, ONON, RXT, SFD, TME. VG, VSTS

- Economic data:

- US: ADP Weekly change, Existing Home sales,

- Global: Brazil inflation, Mexico Industrial production

- Central Banks:

- Rate Decision: Reserve Bank of Australia

- Auctions: US 6w/3yr

- Energy: API Crude Inventories (AMC)

- Earnings After-Market: CAVA, CRWV, FLY, HRB, LITE, QNT, SMCI

- Wednesday -

- Earnings Pre-Market: AMCR, EAT, EYE, KTB, NBIS, PFGC, SLAB, TORO, WRD

- Economic data:

- U.S: Mortgage Apps, CPI

- Global: India Inflation

- Central Banks:

- None

- Energy: EIA Inventories, OPEC Monthly Report

- WASDE Report

- Auctions: 10yr, Germany 30yr

- MSCI Index Review Announcement

- Earnings After-Market: AOSL, BTGO, CAE, CBRS, COHR, CSCO, DOX, ENS, EQPT, GO, HLIT, INFQ, JACK, NNE, PAR, REZI, SECZ, SPCE, STAA

- Thursday -

- Earnings Pre-Market: AIT, AUPH, BIRK, BN, DDS, FRMI, JD, LAC, LUNR, PS, SSYS, TPR, WWW, XE, YETI

- Economic data

- US: Jobless claims, PPI

- Global: Japan PPI, UK Industrial Production/GDP, EU industrial production

- Central Banks:

- Speakers: Fed Barkin, Hammack

- Fed Balance Sheet

- Auctions: 4/8w

- Energy: EIA Natural Gas Inventories

- Earnings After-Market: AMAT, GEMI, GSAT, GLOB, MFP, ROST, YSS

- Friday - 13f's Due

- Earnings Pre-Market: None

- Economic data

- US: Retail sales, U of Mich. Sentiment (prelim), Business Inventories

- Global: China Loan Growth, South Korea import/export prices, Germany wholesale prices, India wholesale prices

- Central Banks

- Fed Commercial Bank Balance Sheets

- Auctions: South Korea 50yr

- Energy: Rig Count

- CFTC COT

- Earnings After-Market: None

Connect with NYSE

By submitting this form you hereby expressly grant permission to use the information included thereunder to contact you for the purposes of sending periodic updates about ICE and/or its affiliates. Certain indices mentioned above are administered by ICE Data Indices, LLC.

Your contact information will not be used for any purpose other than that for which your consent has been given. To learn more about our privacy policy, please click here.

© 2024 Intercontinental Exchange, Inc. All rights reserved. Intercontinental Exchange and ICE are trademarks of Intercontinental Exchange, Inc. or its affiliates. For more information regarding registered trademarks, limitations, restrictions, and other important information, please visit intercontinentalexchange.com/terms-of-use.